》View SMM copper quotes, data, and market analysis

》Order and view SMM metal spot historical prices

》Click to view SMM copper industry chain database

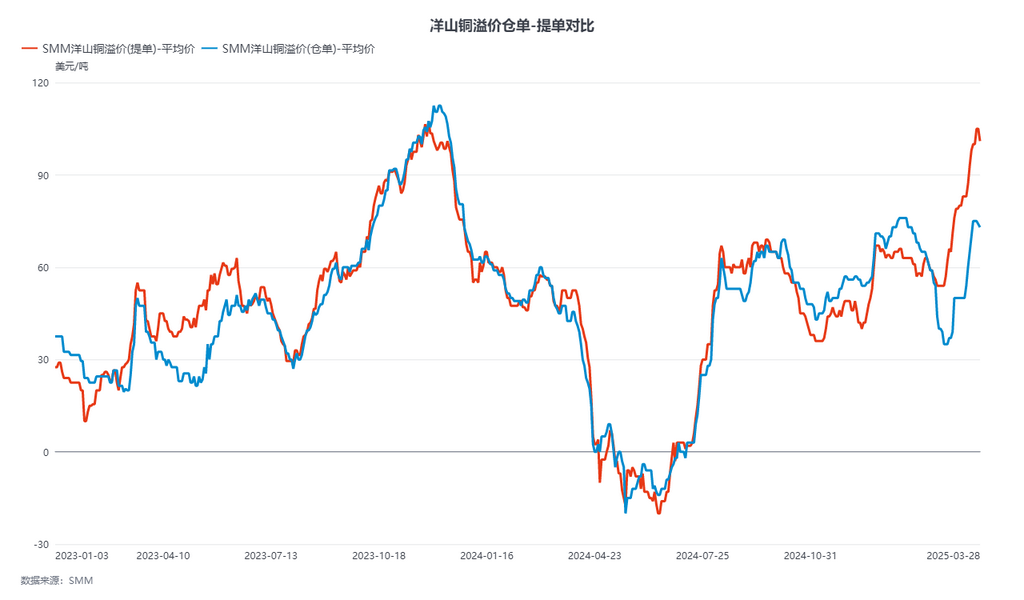

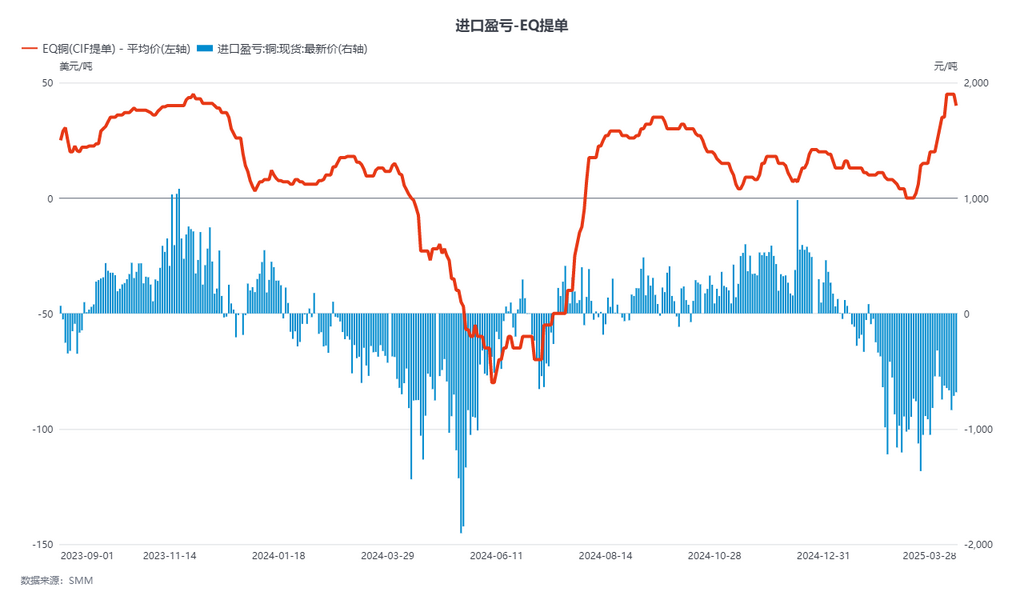

This week (March 24-March 28), the weekly average price range of Yangshan copper premiums for B/L transactions was $97.2-$107.2/mt, QP April, with an average price of $102.2/mt, up $13.4/mt WoW. Warrant prices were $70-$78.8/mt, with an average price of $74.4/mt, up $14.6/mt WoW, QP April. EQ copper CIF B/L prices were $39-$49/mt, with an average price of $44/mt, up $15/mt WoW, QP April. As of March 28, the SHFE/LME price ratio for LME copper to SHFE 2504 contract was 8.20, with import profit/loss around -800 yuan/mt. As of Friday, LME 3M-Apr copper was at C$23.69/mt; the spread between April and May date swap fees was C$18.45/mt.

Currently, the spot price for high-quality ER copper warrants is $76/mt, mainstream pyrometallurgy at $73/mt, and SX-EW at $70/mt; high-quality copper B/L at $106/mt, mainstream pyrometallurgy around $101/mt, and SX-EW at $96/mt; EQ copper CIF B/L at $35-$45/mt, with an average price of $40/mt.

This week, the spot market tended to be quiet, with supply-side disturbances continuing. At the beginning of the week, due to market rumors of production cuts at Altonorte and SPCC-ILO smelters, the offer prices for long-term B/L remained firm. As a result, some B/L originally destined for Southeast Asia from Japan and South Korea flowed to China. In mid-week, concerns about the US reciprocal tariff policy and the accelerated implementation of copper tariffs resurfaced, leading to quiet B/L transactions in the market. As domestically sourced goods canceled from LME arrived at ports, warrant prices also peaked and pulled back. In the short term, buyers' purchase willingness is low, and the upward momentum of Yangshan copper premiums has started to weaken after two consecutive months of climbing, with a heavy market wait-and-see sentiment. However, based on the 250,000-300,000 mt of copper cathode arrivals in the US from March to April, the supply of copper cathode in Asia will remain tight after entering Q2.

According to the SMM survey, as of Thursday (March 27), domestic bonded copper inventories increased by 5,800 mt WoW to 78,900 mt. Among them, Shanghai bonded inventories increased by 6,200 mt WoW to 69,500 mt; Guangdong bonded inventories decreased by 400 mt WoW to 9,400 mt. Bonded inventories continued to increase this week, putting pressure on the premiums for bonded copper cathode. Warrant price offers have shown a pullback trend, and as B/L continuously canceled from LME Asian warehouses arrived at ports, both imports and exports were active. Therefore, bonded inventories showed strong liquidity. It is expected that bonded inventories will continue to increase next week.